Here is the working list of things crypto treats as proof of trustworthiness, with what each one measures and what it borrows when used as a trust indicator instead. What we mean is that the signal itself contributes nothing to risk. Instead, it wires a project to a trusted entity, and the wire is cheap.

Market cap. Borrows credibility from "the market." Measures price times circulating supply. Does not measure whether anyone would buy the next $10M of supply at anything close to that price.

TVL. Borrows credibility from "users have voted with their capital." Measures dollars locked in a contract at current prices. Does not measure whether that liquidity is sticky, mercenary, double-counted across protocols, or paid for with the project's own freshly minted token. A protocol can buy its own TVL with incentives and call it adoption.

Trading volume. Borrows credibility from "lots of people are trading this." Measures transactions, not organic ones. A Columbia University study published in November 2025 estimated that in some weekly windows, almost 60% of Polymarket volume was inauthentic, with one cluster of 43,000+ wallets generating nearly $1M in volume mostly at sub-cent prices, almost all flagged as likely wash trades. Polymarket is one of the more visible platforms in crypto.

Audit badge. Borrows credibility from the audit firm. Measures that a security firm reviewed a version of the code, on a specific date, against a specific scope. Does not measure whether the dependency changed, whether the multisig was migrated, or whether the team kept the practices. An audit from February did not stop a $285M drain in April.

KYC and "verified team." Borrows credibility from "a regulator-style process happened." Measures that a third party saw a passport. Does not measure whether the team is competent, honest, or still the same people holding the keys.

Partner logos. Borrows credibility from the named partners. Measures that someone, somewhere, signed something. The "backed by" wall is the most lawyered, least informative element on most landing pages. A venture firm holding tokens it acquired in a seed round in 2022 is still on the logo wall in 2026 even after it has fully exited.

Follower counts, engagement, GitHub stars. Borrows credibility from "look how many people cares." All purchasable. There is a market for each one. (You can quote us on X on this when the next 200k-follower "DeFi protocol" rug pulls.)

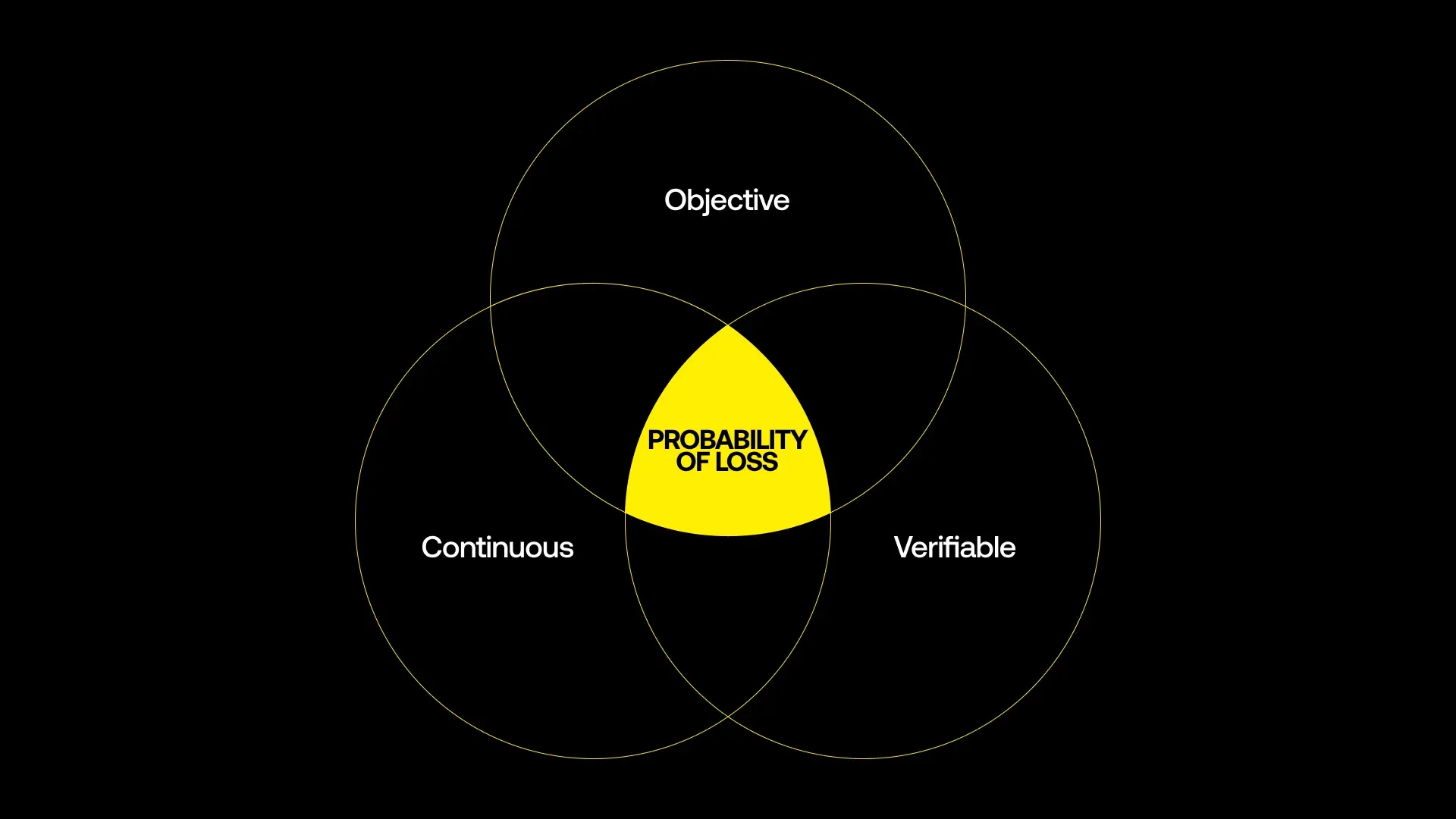

Each of these started as a reasonable proxy for something. Then someone figured out how to spike the proxy without changing the underlying thing. *You’re here*