The best risk-adjusted positions are a small group of vaults that pay double-digit yields while carrying only moderate issuer risk, roughly the same risk level the market is currently accepting low single-digit yields for elsewhere.

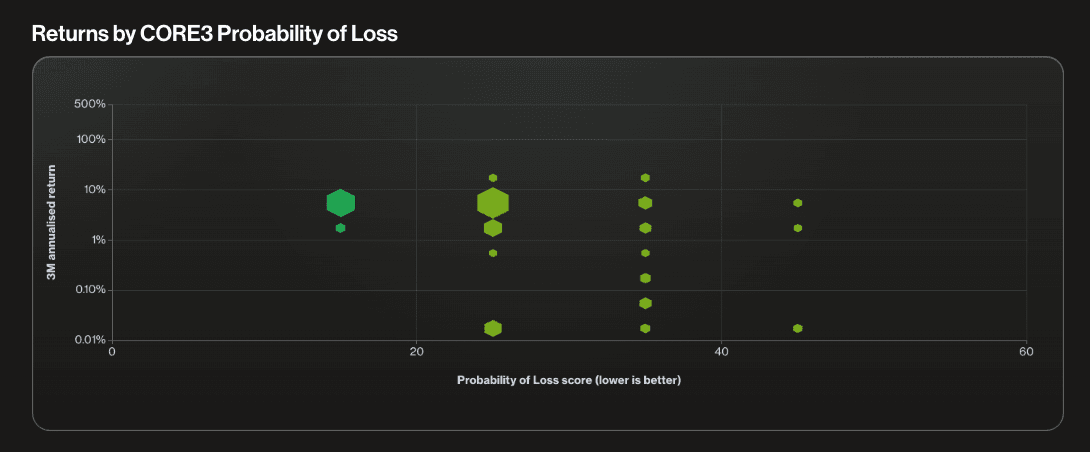

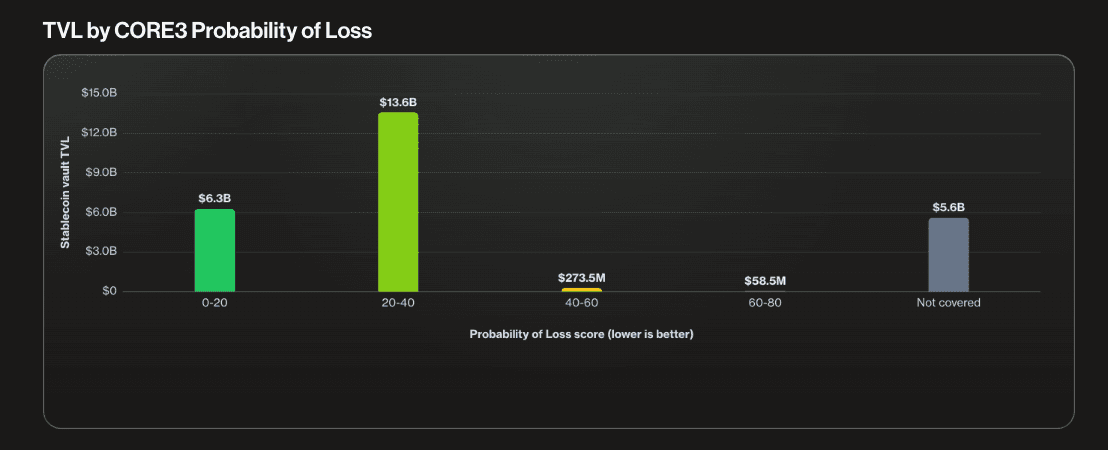

To read the figures below: PoL (Probability of Loss) is an issuer-risk score where lower is safer. TVL (Total Value Locked) is the amount of capital deposited. The return shown is the trailing three-month yield, annualized.

Two standout positions:

First, a cluster of 19 vaults at a PoL score of 24 and 12.3% APY. It holds $62.9M in total, with the largest positions being Alpha USDC Delta V2 (Morpho) at $22.2M, Api3 dCOMP USDC (Morpho) at $8.1M, and Alpha USDC Asia V2 (Morpho) at $7.7M. Its significance is that the issuer risk is nearly identical to a much larger $8.2B cluster that pays only 4.0%, yet this group pays ~three times the yield.

Second, a cluster at a PoL score of 36.0, paying 11.7%, holding approximately $104M. This is the second pocket of double-digit yield available at moderate risk.

For context, the largest default position is Sky's USDS vault: $5.9B in TVL at a PoL score of 13, paying 3.7%. This is the lowest-risk option available and is priced accordingly. It is appropriate for capital preservation rather than yield generation.

Why these positions stand out: across the broader market, yield does not increase as risk increases beyond a PoL score of 40. In other words, taking on more issuer risk above that level does not earn a higher return. The opportunity is therefore concentrated in these specific moderate-risk clusters rather than spread evenly across the risk spectrum. The PoL 24.4 and 36.0 clusters are notable precisely because they offer double-digit yield without a meaningful increase in risk.

One important qualification: these clusters are small, averaging only a few million dollars per vault. As a result, deploying significant capital into them may compress the yield, and the ability to exit quickly during market stress is a genuine consideration that the risk score alone does not capture. The figures should be treated as directional rather than as evidence of capacity to absorb large allocations.